Have you ever read through a 30 – 40 page Trust and really understood how it worked? Even the brightest individuals have a difficult time deciphering a trust if trust law is not their area of expertise.

That’s why we decided to create Trust Charts for our estate planning clients, and share them here for others to take a look at.

If we’re doing your estate plan (or simply your trust), we can provide a custom chart that mirrors your individual trust and distribution plan. For our purposes here, however, we’re sharing a more general example of how assets in a trust flow through sub trusts upon the death of one of more “Settlors”, and how those assets eventually get distributed to beneficiaries.

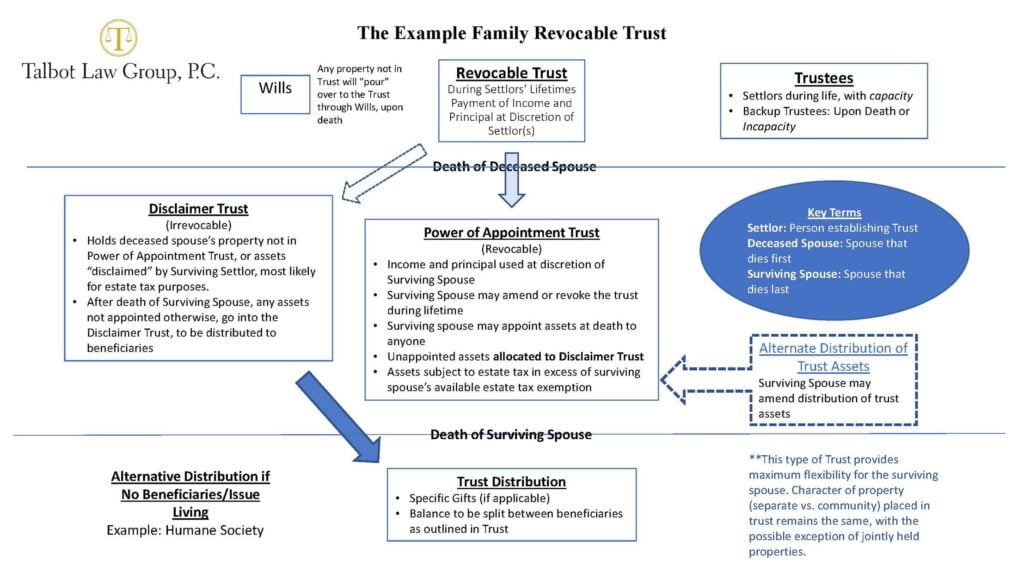

So, let’s take a look at the chart pictured above. If you want to expand it, just click on the image.

This is a California revocable trust for a married couple. This trust maximizes flexibility for the settlors (people establishing the trust) during their lifetimes, and after the first of them dies. Note that this is just one way to do a joint revocable trust, and is only an example for purposes of illustrating the general concept of trust distribution in California (ie not legal advice).

So, now that we’ve got that bit of legalese ironed out, how does the “Example Family Trust.,” pictured above, work? Well, you’ll see at the top of the chart a box labeled “Revocable Trust.” The Revocable Trust is the bucket where the settlors (Mr. & Mrs. Example) place their assets, such as bank accounts and property (real estate and personal). All property and accounts remain in the settlors’ names as trustees of their trust – i.e. Mr. Example and Mrs. Example, Trustees of the Example Family Trust (for example).

At some point, hopefully after Mr. and Mrs. Example have lived a long full life, the first of them dies. In the chart, you’ll see “Death of the Deceased Spouse” represented by a horizontal line. When the first spouse dies, all of the assets in the revocable trust bucket generally pass to what is called the “Power of Appointment Trust.” It’s called the Power of Appointment Trust because the surviving spouse has the power to appoint the assets in the trust as he or she sees fit. The surviving spouse might, however, choose to “disclaim” some of the assets for tax purposes or other reasons, in which case those assets would be placed in the “Disclaimer Trust”. We don’t see disclaimer trusts being used too often, however, especially given the high federal estate tax limit.

Nevertheless, the Disclaimer Trust Provision is important (at least in this trust), because it spells out how the assets are to be distributed upon the death of the second spouse. A little counterintuitive perhaps – but keep reading.

Now, let’s assume that Mr. Example dies first (yes, women do tend to live longer). The trust assets now belong to Mrs. Example, and to keep it simple, are held entirely in the Power of Appointment Trust. Mrs. Example has two options – either she keeps the current beneficiary distribution plan as decided by herself and Mr. Example, or she changes the distribution plan. If Mrs. Example makes no changes, then at her death all of the assets are distributed pursuant to the terms set forth in the Disclaimer Trust, just as Mr. and Mrs. Example had planned for. In the chart, you can imagine all of the assets passing out of the Power of Appointment Trust and into the Disclaimer Trust, before moving to the “Trust Distribution” box pictured at the bottom. If Mrs. Example decides to appoint half of the assets in the Power of Appointment trust differently, then those assets do not pass to the disclaimer trust but instead are distributed according to a different scheme, outside the scope of our chart. Now, keep in mind, in this scenario where we have assets moving from the revocable trust to the Power of Appointment Trust to the disclaimer trust, the assets are not actually moving from trust to trust or being retitled. The purpose of “imagining” the assets moving from bucket to bucket is to understand how the assets are distributed, and if that distribution can be changed (distribution can be changed in the Revocable Trust and the POA Trust, but not the Disclaimer trust).

Now, if you’re not overwhelmed by information yet, you might be wondering why many married couples choose to set up their trusts in such a way that the surviving spouse could completely change the distribution scheme when the first of them dies. It might seem more sensible for the trust to be set up in such a way that locks in the distribution plan – thereby not allowing the surviving spouse to make sweeping changes, such as giving everything to the pool boy (!). Certainly trusts can be done like this – it’s commonly known as an “AB” or “ABC” Trust. In an AB Trust, part of the trust becomes irrevocable upon the death of the first spouse. Irrevocable = no changes can be made. However, there are downsides to this, such as potential tax consequences, that most couples with children in common ultimately choose to avoid.

So, what’s the bottom line? If you’re in a relationship where you wish for the other person to inherit your assets when you die, and you trust that he or she will provide for the beneficiaries you have chosen, this is the simplest, most flexible way to set up your living trust. You avoid probate, you avoid confusion over where assets are and how they are held, you clarify who gets those assets upon your death, and you provide flexibility for your spouse if you should die first.

If you’re curious about the AB Trust, or ABC Trust, stay tuned for a future post. We’ve got a chart for that too.

If you would like to set a consultation for your estate plan, contact our California Trust and Estate Law Firm at 925-322-1795.